Table of Content

While both products let you use your equity to your advantage, a home equity loan gives you a one-time lump sum of money. While a home equity line of credit provides convenient ongoing access to funds for current or future needs. RBFCU operates more than 60 branches in Texas, and it provides home equity loans and lines of credit to eligible members who own property in the Lone Star State. You may take steps to strengthen your credit score by making consistent on-time payments on your credit accounts, keeping your balances low and following other credit-improving tips.

Borrowers taking out less than $175,000 against their home won’t need to pay appraisal fees. However, requesting larger home equity loans and lines of credit may mean paying for some or all of the home appraisal. Opinions expressed here are author's alone, not those of any bank, credit card issuer or other company, and have not been reviewed, approved or otherwise endorsed by any of these entities. All information, including rates and fees, are accurate as of the date of publication and are updated as provided by our partners. Some of the offers on this page may not be available through our website. A home equity loan or line of credit provides access to larger loan amounts than you may otherwise be unable to get, thanks to using your home as collateral.

Differences from conventional loans

Additionally, if you close your account within 36 months, you’ll be on the hook for the closing costs PenFed paid on your behalf. There’s also a $99 annual fee (waived if you paid $99 in interest in the previous year), and you may have to pay taxes in certain states and appraisal fees if an appraisal is required. A home equity loan is similar to a HELOC in that it is a loan that is offered by a lender based on your home equity.

May include additional fees, such as cancellation fees, annual fees, application fees, appraisal fees and closing costs. However, lenders may also look at other qualifying factors to determine exactly how much credit to extend. These might include credit scores, credit history and debt-to-income ratios.

Chase Home Lending

Visit our mortgage education center for helpful tips and information. And from applying for a loan to managing your mortgage, Chase MyHome has you covered. We offer a variety of mortgages for buying a new home or refinancing your existing one. Our Learning Center provides easy-to-use mortgage calculators, educational articles and more.

As long as you have equity—your home’s current value is greater than what you owe on the property—you may be eligible to tap into it. Although you may have heard that the interest on home equity loans and HELOCs is usually tax deductible on loans up to $100,000, that's not quite the full picture. In truth, the interest you pay on a mortgage up to $1 million is tax deductible. If you have a home equity loan, that overall mortgage limit gets bumped up by $100,000 to $1.1 million, according to Rob Seltzer, a CPA who runs a firm bearing his name in Los Angeles.

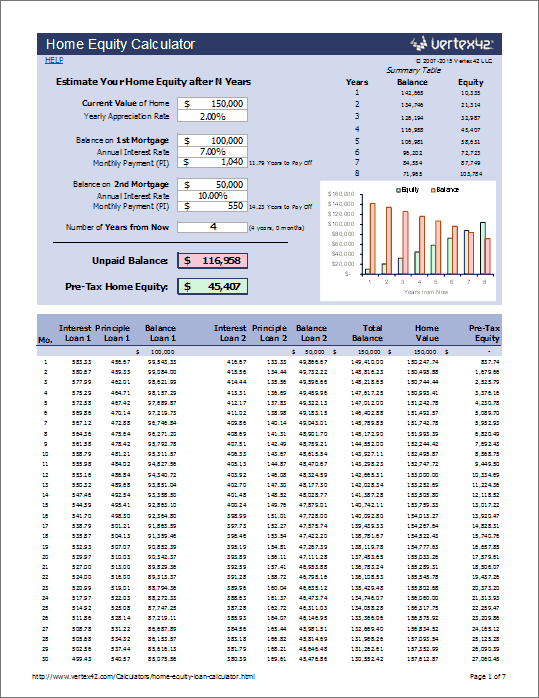

Home Equity Loans

The amount of credit available to you is dependent on the equity in your home, your credit score, and your debt-to-income ratio. Because HELOCs are secured by an asset, they tend to have higher credit limits and much better interest rates than credit cards or personal loans. While HELOCs usually have variable interest rates, there are some fixed-rate options available. This type of financing, also known as a HELOC, is a revolving line of credit, much like a credit card except it is secured by your home. Generally, as long as you stay under that credit limit, you can borrow as much as you need, any time you need it, by writing a check or using a credit card connected to the account. Many HELOCs have an initial period of time — a draw period — when you can borrow from the account.

Skylar Clarine is a fact-checker and expert in personal finance with a range of experience including veterinary technology and film studies. If you think your lender has violated the law, you may want to contact the lender or servicer to let them know. At the same time, you also may want to contact an attorney. Avoid a lender who wants you to apply to borrow more than the amount you need. What to know when you're looking for a job or more education, or considering a money-making opportunity or investment.

Regardless, using a home equity line to pay for a vacation or to fund leisure and entertainment activities is an indicator that you’re spending beyond your means. It’s cheaper than paying with a credit card, but it’s still debt. If you use debt to fund your lifestyle, borrowing from home equity will only exacerbate the problem. At least with credit cards, you are only risking your credit—with a HELOC, your home is at risk. A cash-out refinance replaces your original mortgage with a new, bigger one. Since you’re borrowing money against the equity, that amount is rolled into your new mortgage.

If the real estate values decrease, your home market value could also decrease. If you’re planning to sell your home during this time, you may lose money on the sale. Beware, though, that when you use a HELOC to consolidate credit card debt, you’re trading an unsecured loan for one that’s secured by your home.

You are now leaving Mid Minnesota Federal Credit Union's website. MMFCU is not responsible for the content or availability of linked sites. Please be advised that MMFCU does not represent either the third party or you, the member, if you enter into a transaction. Further, the privacy and security policies of the linked site may differ from those practiced by the credit union. Having your insurance coverage on file with Mid Minnesota saves you money. If you change insurance carriers or recently bought your vehicle, update your insurance information to keep your payment low.

Maybe you can’t handle seeing your investments drop overnight or you will be retiring soon and can’t handle this amount of volatility. One problem with crypto investments is that people often dive in without knowing much about it. Crypto and other alternative investments may not be a bad choice if you know what you’re doing, so educating yourself first is important. And that’s true whether you’re buying highly speculative crypto or more established investments such as index funds. We’re transparent about how we are able to bring quality content, competitive rates, and useful tools to you by explaining how we make money.

That will generate extra money for things like home improvements, college tuition or your kid’s wedding. Your home equity is the portion of your home that you own outright . And collateral is the security for your loan—in other words, it’s the thing you promise to give to the lender if you can’t pay back what you owe.

HELOC interest rates tend to be lower than interest rates for home equity loans and personal loans. However, HELOC rates also tend to be variable, meaning that rates could increase depending on decisions from the Federal Reserve. As rates continue to rise, a HELOC with a variable interest rate might be a riskier proposition for some. Interest paid on a HELOC istax deductibleas long as it’s used to “buy, build or substantially improve the taxpayer’s home that secures the loan,”according to the IRS. So if you had a $600,000 mortgage and a $300,000 HELOC for home improvements on a house worth $1.2 million, you could only deduct the interest on the first $750,000 of the $900,000 you borrowed.

Choosing an interest-only repayment may cause your monthly payment to increase, possibly substantially, once your credit line transitions into the repayment period. Repayment options may vary based on credit qualifications. Loans are subject to credit approval and program guidelines. Not all loan programs are available in all states for all loan amounts. Interest rates and program terms are subject to change without notice. Credit line may be reduced or additional extensions of credit limited if certain circumstances occur.

No comments:

Post a Comment